The Japan Carry Trade Unwinding

In the US there are prime brokers (Morgan Stanley, Goldman etc) who are able to borrow Yen from Japanese banks. Hedge Funds, who must have US$ on deposit with their primer broker, then borrow the yen at the prevailing...

Lynk

Lynk

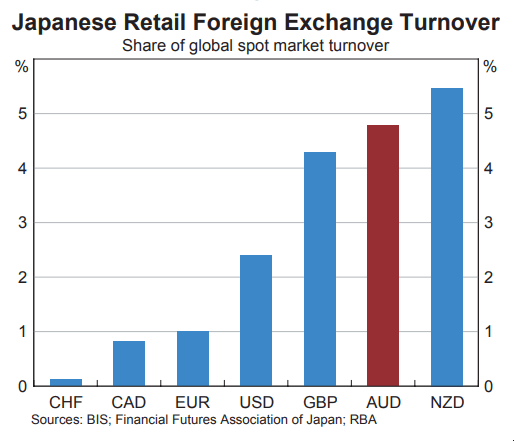

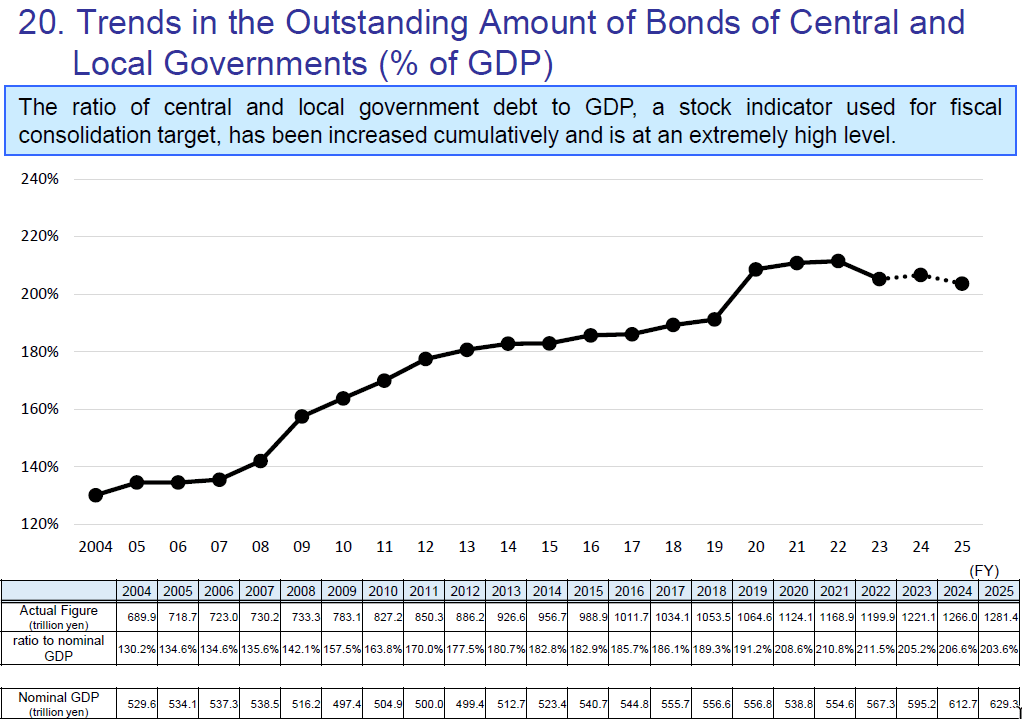

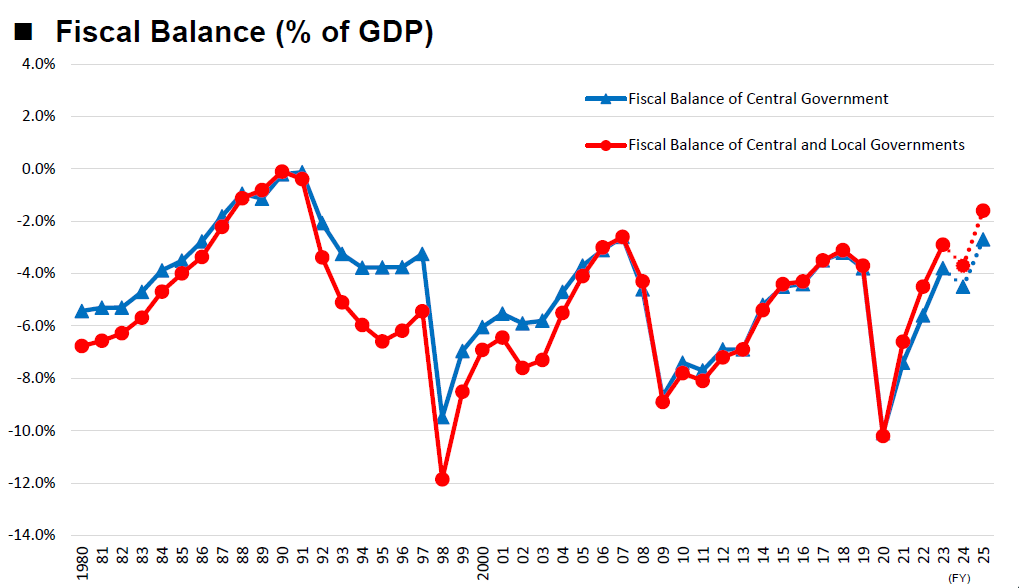

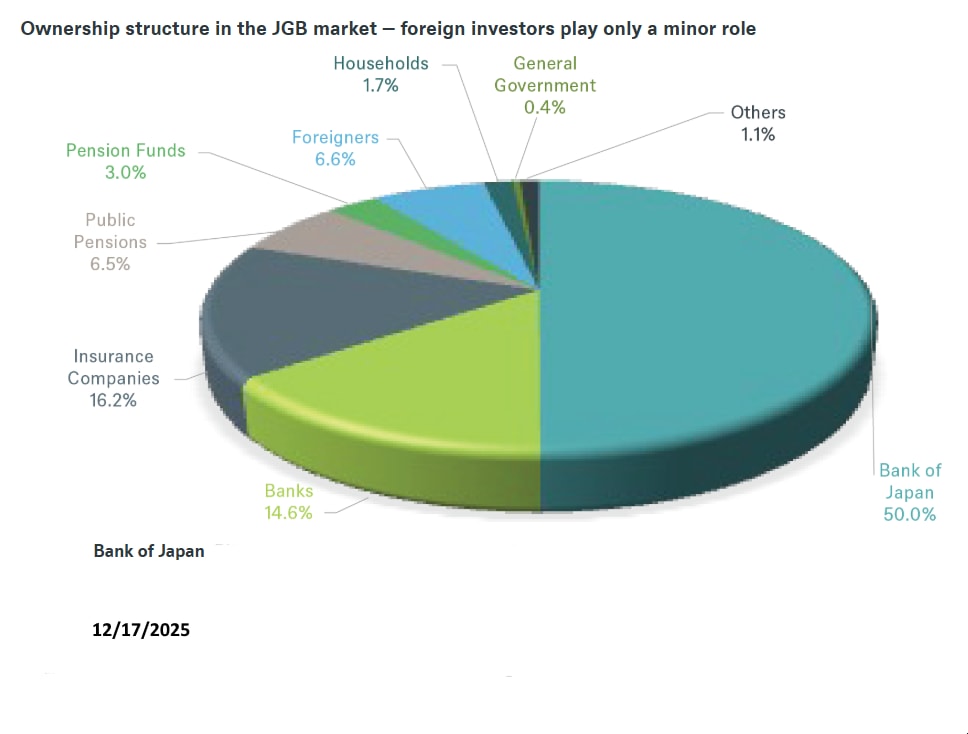

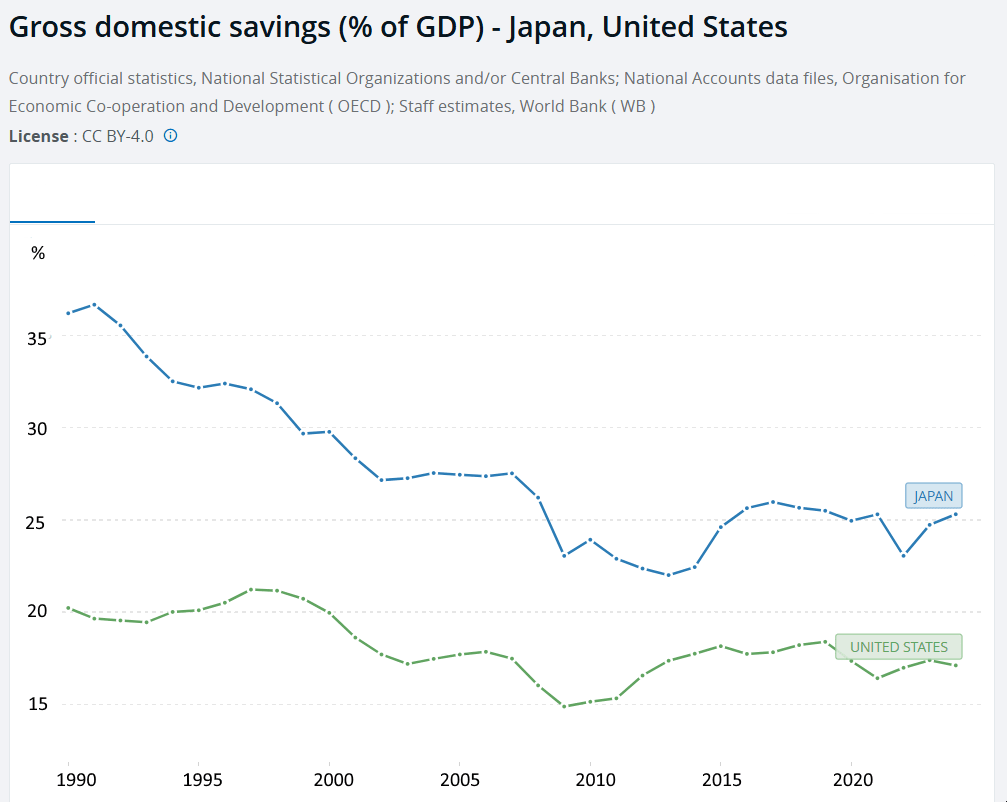

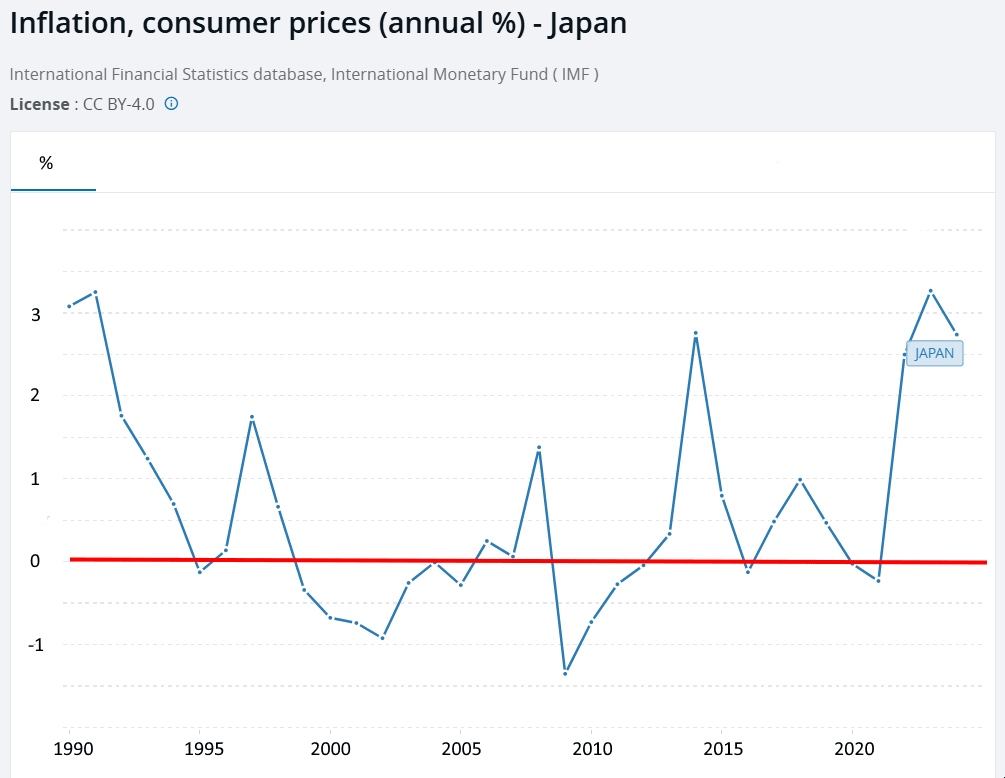

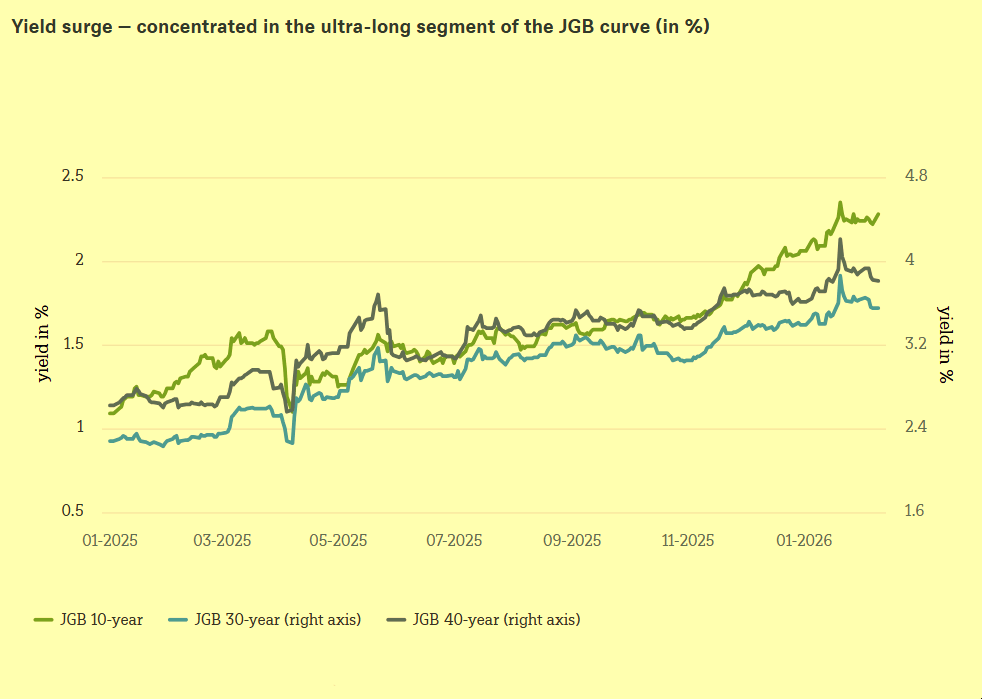

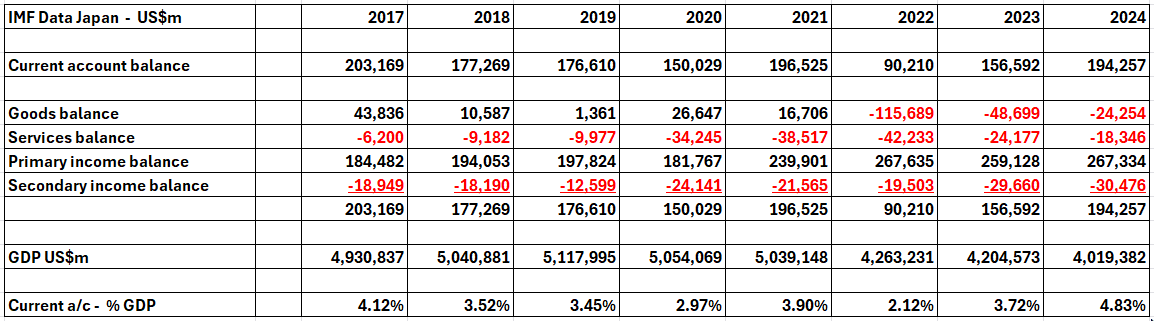

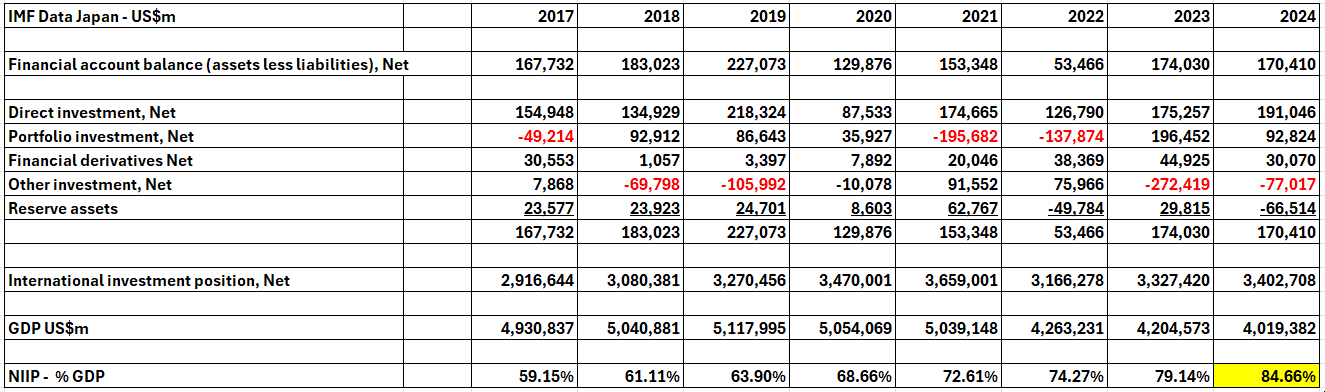

For long periods the Bank of Japan (the Central Bank) was known to pursue a policy of exchange rate stability such that movements in the US$/Yen rate occurred abruptly and the timing could be anticipated and this significantly reduced the exchange rate risk in the carry trade. Were a Hedge Fund to purchase a futures contract to protect against exchange rate shifts then the cost of the contract would be more or less the same price as the interest differential in the carry trade so it would not make sense. What has happened in Japan in the last year or two is that interest rates have risen such that the profitability of the carry trade has reduced. Does it matter if Hedge Funds start to abandon this strategy in terms of the overall economy. Obviously an abrupt shift (such as a sharp appreciation of the Yen) would put many carry trades underwater with the potential to bankrupt their sponsors with knock-on effects in the wider economy. Clearly, this is not going to occur in this case. The other carries are by domestic Japanese retail and institutional investors. They have been investing offshore for decades to profit from the interest differentials with other currencies such as the USD, CAD, AUD, NZD etc. In this case the Japanese investor is not “hedged” but does have a currency risk in the event of yen appreciation. In recent decades the Japanese economy has been categorized by: At the time of writing the Government needs either higher inflation or lower State deficits in order to bring the debt/gdp ratio down. Deficits are running at 5-6% of GDP with little prospects for a reduction and that means that the solution is higher inflation. This is pure arithmetic. Japan cannot realistically continue to let the debt/gdp ratio climb since it is already the highest in the world. The causes of low inflation in Japan has long been debated especially given that the Bank of Japan holds about half of all Government debt. That is, the Central Bank has been lending the Government money for its day to day expenses. In almost any other country what amounts to printing money would have led to a spike in inflation but this did not occur in Japan. What is peculiar to Japan is the high savings ratio which meant that people saved rather than spent, the Current a/c surplus which meant that surplus savings could find a home abroad and tight Government controls and subsidies which affect consumer prices. Inflation since the bubble burst in 1990 has often been negative though there has been an uptick in the last few years. Long term interest rates have started to climb from very low levels in the last year. Japan’s Current a/c surplus is mostly attributable to Primary Income surpluses (investment income). At end 2024 Japan had a positive Net International Investment Position of 85% of GDP (i.e. what it owns abroad vs what rest-of-world owns in Japan) as per the IMF data. To conclude: Read our full report at - https://www.marketresearch.com/Latin-Report-v4296/Economy-Japan-43065791/ Paul Dixon is the founder of Latin Report. His economics articles on a wide variety of topics are very widely read and are often found ranking in search results for months and even years after being first posted. Latin Report tries to make sense of the vast volume of information available to understand country economies. Our reports are written from a long term perspective and track a country's evolution over a number of decades. We mostly let the data tell the story with commentary on political events to illuminate features of the data. Latin Report aims to express views that hold their value over time and should therefore assist companies making long term decisions. This compares to competitors' reports based on current analysis which are subject to continual revision. https://latinreport.eu In the US there are prime brokers (Morgan Stanley, Goldman etc) who are able to borrow Yen from Japanese banks. Hedge Funds, who must have US$ on deposit with their primer broker, then borrow the yen at the prevailing interest rate which was usually near zero for several decades. The Yen are converted into US$ and invested at the prevailing US$ rate of, say, 3-4%. Thus the Hedge Funds earn the interest rate differential between the Yen and Dollar but assume a risk of adverse currency movement.

In the US there are prime brokers (Morgan Stanley, Goldman etc) who are able to borrow Yen from Japanese banks. Hedge Funds, who must have US$ on deposit with their primer broker, then borrow the yen at the prevailing interest rate which was usually near zero for several decades. The Yen are converted into US$ and invested at the prevailing US$ rate of, say, 3-4%. Thus the Hedge Funds earn the interest rate differential between the Yen and Dollar but assume a risk of adverse currency movement.