While Luna burns, not all hope is lost: Lessons that Terraform Labs can learn from

As Terraform Labs struggles to rebuild its crypto ecosystem, what can it do to make the Terra-Luna system stronger than before?

Hollif

Hollif

Disclaimer: Opinions expressed below belong solely to the author.

When Do Kwon tweeted the now-famous line “I don’t debate the poor”, his pet projects Luna and Terra were doing extremely well.

Image Credit: Reddit

Image Credit: RedditBut as they say, the bigger they are, the harder they fall, and the crash of these two tokens was no exception.

A typically brash, proud, and arrogant Do Kwon tweeted a humble apology to his community of LUNATICS, and promised to try and fix what destruction his invention had wrought upon the MetaMask accounts of his supporters.

From the heights of more than US$110 per token, the tokens’ value plummeted to become almost worthless overnight.

The august and glorious no more

Luna and Terra are classified as stablecoins, meaning that their values are pegged to the US dollar.

These coins are supposed to maintain that value, and because they can always be redeemed for something worth at least US$1, stablecoin tokens can (at least theoretically) never go below this peg.

However, the Terra and Luna pair of tokens are special even for stablecoins.

While stablecoins like USDC and USDP are backed by reserves and collateral that can be used to prop up the token if it comes under speculative attack, Luna and Terra are not. Instead, they belong to a special category known as algorithmic stablecoins.

Instead of relying on reserves, these tokens rely on what is effectively a form of arbitrage.

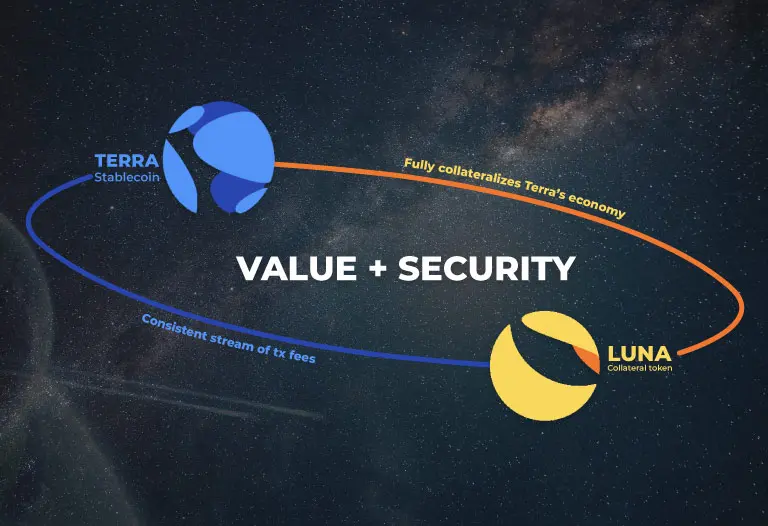

Image Credit: Bitnovo Blog

Image Credit: Bitnovo BlogTerra’s protocol fixes the peg of UST to USD through its counterpart token Luna.

When UST is overvalued, Luna holders can burn Luna tokens to create more UST, with the community taking some of the profit. And when UST is undervalued, UST holders will be incentivised to trade in their UST for the dollar value equivalent of Luna tokens.

Luna tokens by themselves have some utility — they can be staked on the Anchor protocol, providing stakers with income through interest payments, at high interest rates.

In a perfect world, UST would remain permanently stable, pegged at 1 USD, while Luna’s price increases as more users get on board.

But of course, no system is perfect. UST began to give way, and once rumour spread that the coin would be de-pegged from the US dollar, everyone rushed to sell their investments — both in Luna and Terra — and excess demand from the hype quickly gave way to massive oversupply, crashing the value of both tokens.

The original sin of the Terra ecosystem

The design of the Terra and Luna ecosystem is superb. Through seigniorage and algorithmic manipulation, money supply becomes perfectly managed and no longer requires central bank control.

But if the system was indeed perfect, how and why did it fall so spectacularly from grace?

The answer, ironic as it seems, stems from the design of the Terra ecosystem itself.

The entire system relied on the confidence of the public that UST would always remain pegged to the USD at the fixed exchange rate of 1 UST to 1 USD.

When times were good, the ability to exchange UST for USD was never in doubt. But as doubt in the currency peg increased, confidence evaporated and everyone immediately traded in their UST for USD.

As UST was burnt to create Luna, Luna’s prices also decreased and the excess supply and algorithm that had so long kept the ecosystem strong became the very enemy that destroyed it from within.

This cascade of events, known as a death spiral in the crypto space, is analogous to a bank run in real life.

In fractional reserve banking, banks loan out more than they receive, and hold only a fraction of what they lend out in order to pay creditors on demand.

Image Credit: Alt Exploit

Image Credit: Alt ExploitHowever, if too many loans are made, the excess supply erodes confidence in the bank, and creditors begin demanding their money back before the bank goes under. This action, carried out simultaneously by a multitude of creditors, is ironically the very action that eventually drives the bank under and unable to repay all their creditors at once.

Banks that suffer this fate have often made the mistake that they themselves are the guarantor of value, when in reality, it is creditors’ faith in the banks that they will make sound economic and financial decisions.

The mistake by Terra was the same — Do Kwon believed in his system so much that he failed to realise that it was not faith in the ecosystem per se that led to its success. It was faith in the backing of USD that underpinned Terra’s growth, and when that foundation looked like it might give way, the whole mansion came crashing down.

Redemption is still possible

Regardless, that is not to say that the Terra and Luna project is completely useless. I stand by my comment that the design is superb, or at the very least, very promising.

Sopnendu Mohanty, Chief Fintech Officer at the Monetary Authority of Singapore, spoke at Singapore Fintech Festival’s Green Shoots event last week, and addressed the crash with some brief comments. He stressed that we should not let market hype distract us from the real value of innovation in the fintech space, crypto included.

I wholeheartedly agree with this comment. But at the same time, this comment should be applied both in feast time as well as in famine.

We must be careful not to allow the crash in prices to distract us from the innovation that Terraform Labs has presented — a system that unlike Titan and Iron, actually provides a reason for users to stay on the blockchain. But we must also be careful not to allow the hype of the initial success to blind us to the fact that the flaws are not features of the product.

As the community reflects on the problems and solutions for the Terra ecosystem, some inspiration can be drawn from the real world of fiat currency.

While crypto (and Luna in particular) aims to displace fiat currency, the crypto space is nonetheless still in its infancy when compared to the world of fiat. Innovations and lessons taken from the world of fiat economics can still be applied to the world of crypto to make it better.

Firstly, Terraform Labs must understand that it is of paramount importance to restore confidence in their currency peg. Do Kwon at least seems to understand this — as the crash was happening, he was pumping Bitcoin into the system in an attempt to alleviate the excess supply with heightened demand.

This action reveals that he clearly understood what was under attack — the currency peg itself, and it needed to be defended.

But while his attempt was with good intention, his method was inadequate. A problem solution mismatch, if you will.

The attack was taking place because of Terra’s lack of a real backing for its currency peg — the reserves and collateral that USDC and USDP were holding that Do Kwon thought Terra could do without. This was a fundamental mistake, but it can be corrected.

When real world currencies come under speculative attacks, central banks who wish to maintain their currency peg may draw down their reserves and absorb excess supply with heightened demand, but this pool of funds must be accumulated during feast time to be used during famine.

Singapore is a key example. One of the reasons why the Singapore dollar is extremely stable is because of our excessively high national reserves — if the Singapore dollar comes under speculative attack, MAS’ national reserve will more than likely be able to take the hit and more.

Image Credit: IGCSE AID

Image Credit: IGCSE AIDThis idea of the reserve currency underpins confidence in the currency, and if Terra had such a pool of reserves, speculative attacks would be much more difficult.

Another lesson that the Terraform Labs might take from this crisis is that not all economic problems have straightforward solutions. Do Kwon’s system promised to regulate money supply and secure a fixed exchange rate, while simultaneously promising high interest rates and free capital mobility.

But when the markets decided that Terra was not worth holding, the very process that gave the Terra Luna pair strength became its enemy. Despite Do Kwon’s valiant efforts, monetary economics cannot be easily reduced to a single algorithm.

This is a problem of execution rather than of principle — the exchange mechanism did hold under the previous paradigm of confidence in the Terra ecosystem. What remains to be done is to find out what to do when this is not the case, and to automate it such that balance is restored.

With the fall of this next giant of the crypto space, the future of cryptocurrency looks a bit more uncertain once again. However, this is far from the death knell of cryptocurrencies — the technology is proven, but still immature.

Otto von Bismarck once remarked, “Only a fool learns from his own mistakes. The wise learn from the mistakes of others”.

If cryptocurrencies hope to replace fiat currencies, they must also learn from the mistakes of fiat currencies, and ensure that they themselves learn from history. And yet, as Friedrich Hegel notes, “we learn from history that we do not learn from history”.

Hegel also proposed that the ultimate level of human development lies between the extremities of complete freedom and a complete lack of it. Perhaps, with cryptocurrencies pushing the next level of freedom in the financial space, they bring humanity one step closer to this final level of development. Lessons of the past must still be heeded, if we are to actually progress.

Featured Image Credit: Bloomberg