How inflation makes increasing property prices in S’pore a bigger problem than it already is

Singaporean households may be richer, but our youths are not due to high resale, rental and BTO flat prices.

BigThink

BigThink

Disclaimer: Opinions presented below belong solely to the author.

It’s no secret that inflation is probably one of the top concerns for Singaporeans right now.

Inflation this year has hit record levels, and many are wondering how they can cope with it. After all, inflation means that every dollar that you have buys you less than before, including those in our CPF and bank accounts.

Some youngsters are resorting to risky investments like cryptocurrency so that their incomes keep pace with inflation. Additionally, housing is another key concern for many Singaporeans, especially those who have yet to own a piece of property under their name.

Young Singaporeans are also moving towards rentals rather than buying property, and many have cited a lack of savings as a key reason.

Last week, one of our writers opined that households have gotten richer over the pandemic, and that despite the increase in inflation, property values have provided a valuable hedge against inflation.

So what gives? Are Singaporeans better off because of the property prices, or not?

Homeowners have cause to celebrate

Homeownership rates in Singapore are impressive, standing at around 88.9 per cent. This has been a core focus of government policy, and these properties are seen as an asset.

So certainly, property prices in Singapore have generally been on the rise, and the past year has not been an exception. In fact, given how this trend runs counter to global property markets, there are already concerns about a possible property bubble in Singapore.

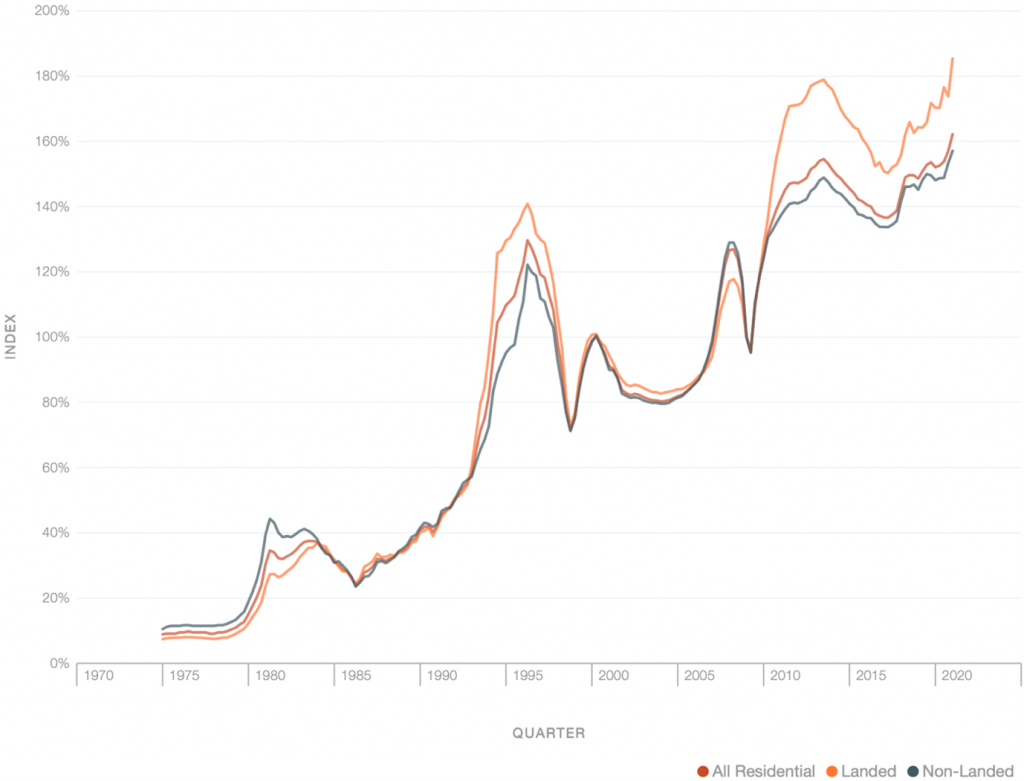

Property price index in Singapore / Image Credit: Department of Statistics Singapore

Property price index in Singapore / Image Credit: Department of Statistics SingaporeLeaving aside the discussion of a property asset bubble in Singapore, rising property prices might be good news. Since the rise in property value outstrips inflation, buying property is generally a good idea to beat inflation and keep your purchasing power.

Homeowners can therefore rejoice, kind of. More valuable property means that you are, at least on paper, richer. But since you cannot exactly spend a house to buy your everyday groceries, the point is also moot.

Homeowners are protected against inflation, but since cashflow factors like income remain unchanged, how much do they actually benefit from this, unless they are willing to sell their property and downgrade?

Many are homeowners, but there are also many who are not

This analysis breaks down when we consider the different types of Singaporeans. As with most economic trends, there is bound to be an uneven impact, so it helps to examine who gains and who loses from the status quo of government housing policy.

While most Singaporeans own their homes, this does not mean that the distribution of those who own their homes is homogenous throughout all age groups.

66 percent of young Singaporeans are choosing to rent instead of buy due to lack of savings. The price of resale HDB flats has also seen an increase, and have doubled since around 2007. As a result, rentals have also seen astronomical growth, and are expected to continue growing.

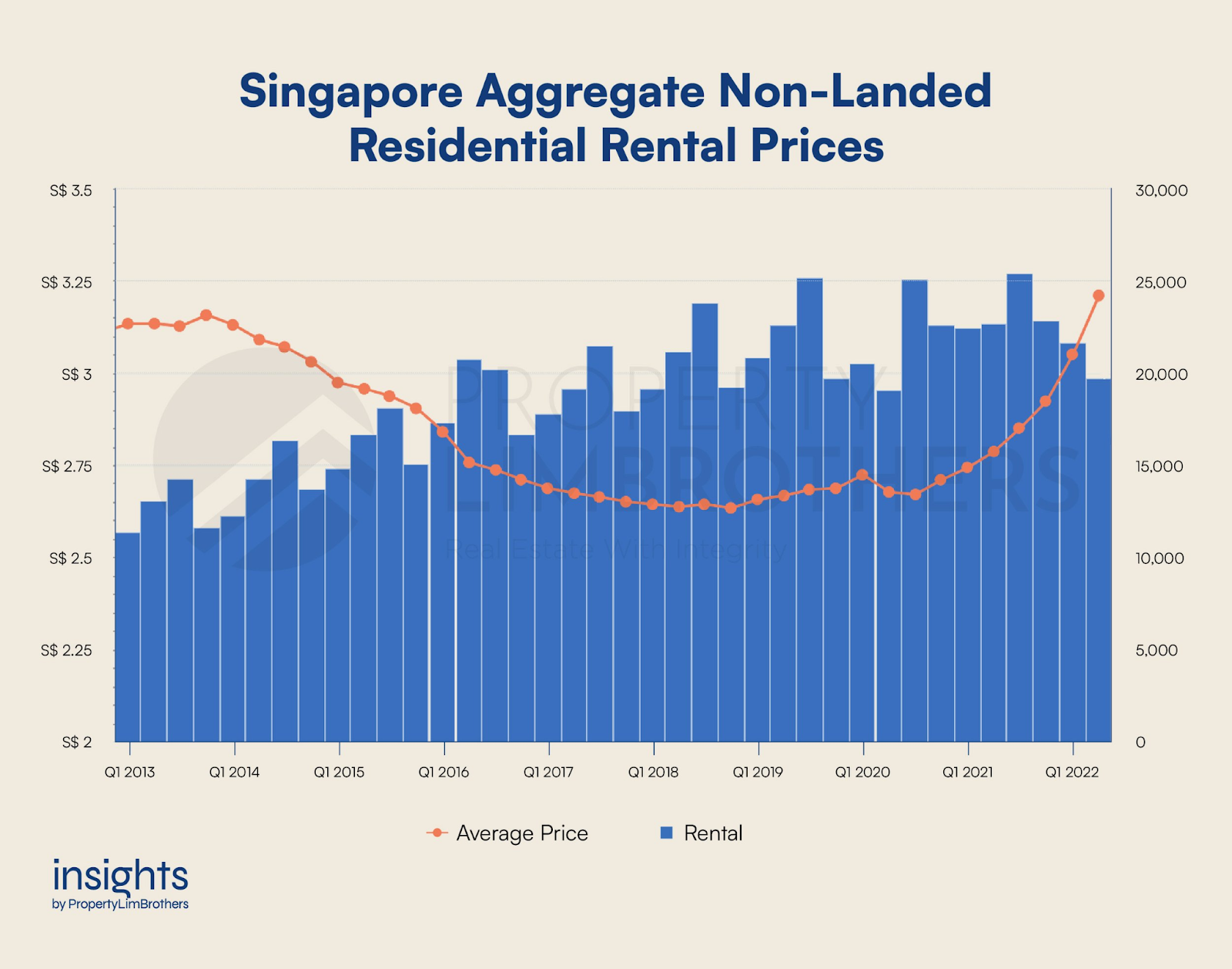

Prices of rentals in non-landed residential areas / Image Credit: Property Lim Brothers.

Prices of rentals in non-landed residential areas / Image Credit: Property Lim Brothers.This means that far from having their properties serve as a valuable hedge against inflation, these Singaporeans have to spend more on their housing needs instead.

Given that 40 per cent of consumers are already seeing their income growth lag behind inflation, this is a serious cause for concern.

Taking stock of all these changes, it means that Singapore’s youths are beset on all sides with challenges — lower savings, higher expenditures, and record inflation are making homeownership less attainable. It’s no wonder that consumer sentiments on property affordability are also dropping.

What about government help?

Singapore has prided itself on its high proportion of home ownership and thus far, a good job has been done.

Part of the reason this has been achieved is that the government offers significant housing grants in addition to allowing Singaporeans to use their CPF to buy new BTO flats.

But have these grants been keeping pace with the rising costs?

The last update to BTO grants was in 2019, not too long ago. But the quantity of the grant indeed leaves something to be desired.

Singles who apply for a resale flat grant can get up to S$80,000, up from the previous amount of S$60,000. Couples or families get double the amount — so as a whole, grant amounts have increased by 33 per cent.

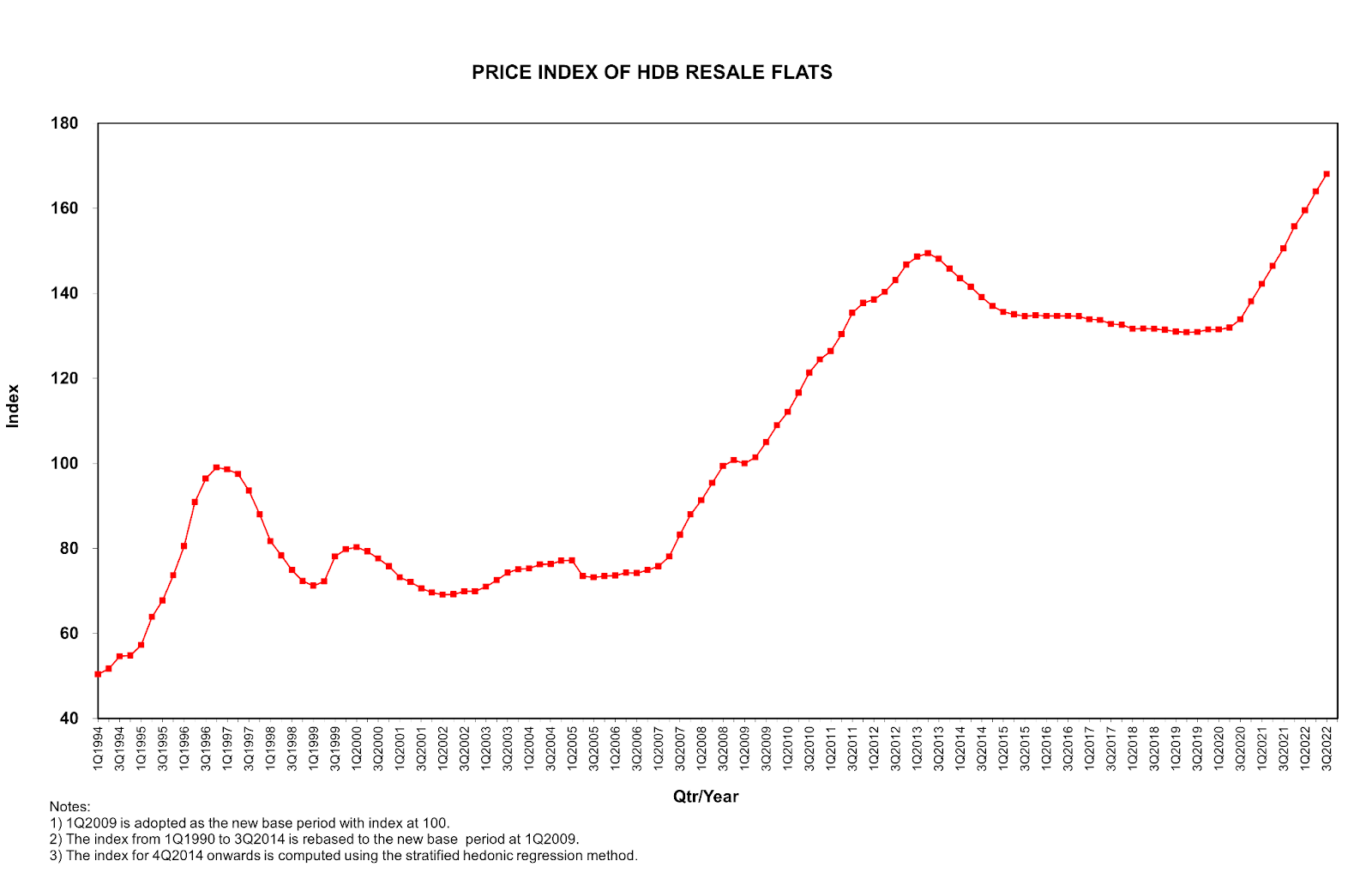

Yet, since 2007, the price index of HDB resale flats has jumped from around 80 to its current high of around 160, meaning that the prices of flats have doubled from around 15 years ago and are continuing to rise.

Price index of HDB resale flats / Image Credit: HDB

Price index of HDB resale flats / Image Credit: HDBUnless grant amounts continue to increase, Singaporeans who hope to own their homes will still have to pay a larger proportion of the total price — and set an even higher threshold for their savings before they can afford to buy.

It’s time to relook housing policy

Despite this, housing policy in Singapore so far has provided most Singaporeans with a roof over their heads, and the ability to own these roofs. For this, we must acknowledge and recognise that housing policy in Singapore has largely been successful thus far.

However, that is not to say that there are no issues to resolve.

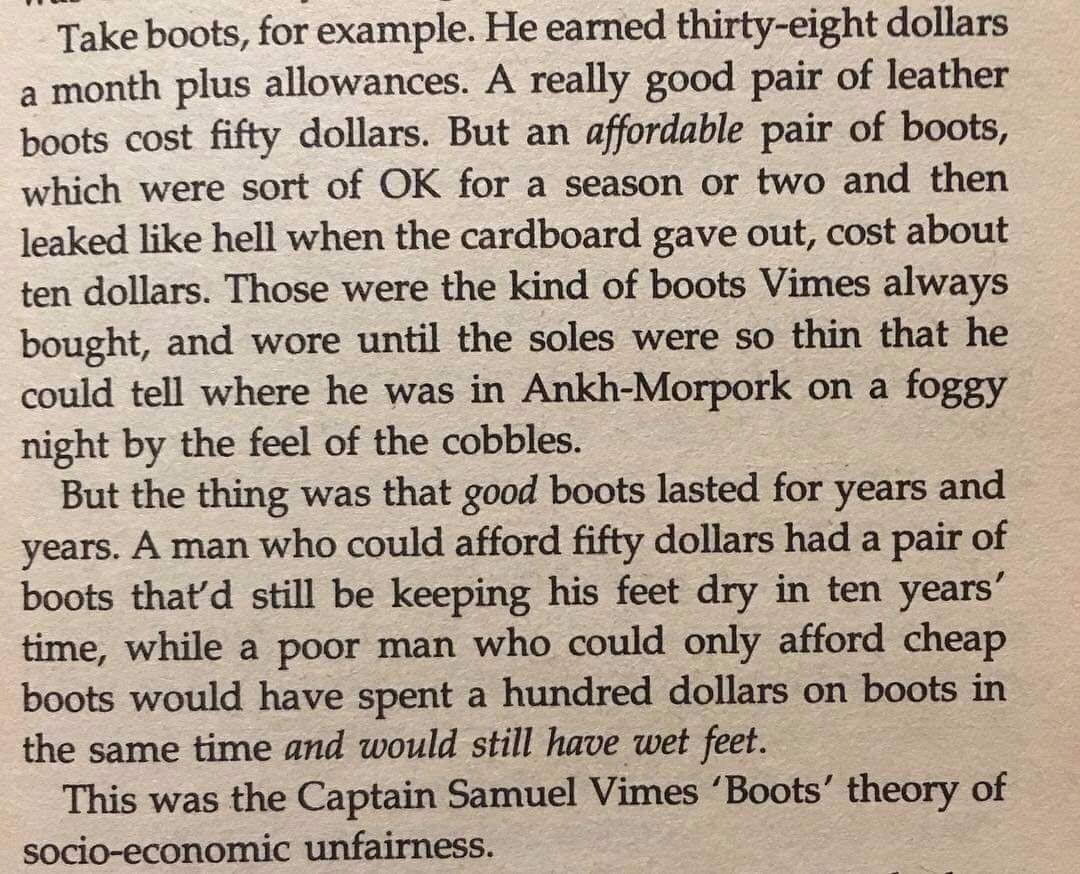

In Terry Pratchett’s novel ‘Men at Arms’, the main character Sam Vimes provides a theory for how the rich stay rich, and at the core of it is the issue of affordability.

Terry Pratchett’s explanation in ‘Men at Arms’ of socio-economic unfairness / Image Credit: Twitter

Terry Pratchett’s explanation in ‘Men at Arms’ of socio-economic unfairness / Image Credit: TwitterIn Singapore’s context, this theory applies to homeowners and renters.

Continually rising housing prices mean that housing is increasingly unaffordable, and as pointed out in the article, renting in Singapore in such a market is probably the best way to become poor.

Since houses are appreciating assets, and grants are not keeping up, the youth are the ones who are forced to foot the bill at the end of the day.

And it is not that the youth do not want to buy, but they simply cannot buy due to the increased prices. With time, this will become extremely problematic.

Since the youth are forced to rent, they cannot save enough to buy, and the market will become dominated by those who continually accrue profits from rents, and allow them to continually amass property to continue bolstering their wealth.

Meanwhile, youths will continue to rent, with no way out of the situation since they cannot afford to buy their homes but still need a place to stay.

Balancing economic incentive with societal needs

That being said, landlords do provide a valuable service to society, since they provide housing for those who would otherwise be unable to afford it.

By buying up property and then renting it out, it makes housing far more liquid — instead of having to buy a house, those who cannot afford to buy can pay to use a small part of the property, and this opens up avenues for the less wealthy to fulfil their housing needs without breaking the bank.

But we should also recognise that there is the possibility of rent-seeking behaviour being taken too far. Landlords who buy extra properties in order to profit from renting are also driving up demand for houses, and causing the increases in price.

Not only do they already benefit from the price increases in the property that they already own, but they also benefit from being able to ask for higher rents when property prices increase. In addition, since they own the properties that they rent out, any benefits from this additional property appreciating in value also accrue to the landlord.

In effect, renters are getting the short end of the stick on multiple fronts, and landlords can enrich themselves at the expense of renters.

Rent seekers refer to those who extract profit without contributing anything meaningful / Image Credit: Steven Conover

Rent seekers refer to those who extract profit without contributing anything meaningful / Image Credit: Steven ConoverSome control may soon become necessary in order to even the playing field. At present, the issue is that housing prices are too high for new prospective homeowners to buy, and this is an issue that needs to be addressed.

But at the same time, we should be careful not to throw the baby out with the bath water.

There are elements of housing policy that remain desirable. Having Singaporeans own their homes, and allowing those who are more well-off to buy leftover properties to rent out, is something that is healthy for the economy.

Instead, it is the worst excesses that such a system allows for that should be curbed.

A flexible cap on rent determined by the cost of the property, for example, could ensure that rents do not climb to astronomical amounts while providing security for the landlord’s investment.

More stringent restrictions on who can apply for new flats and buy new property could also help to reduce any speculative pressure within the property market.

Most significantly, housing needs have to be reprioritised. Having HDB flats and property as an asset for Singaporeans to cash out on in the future is good and desirable, but attaining this goal should not come at the expense of citizens not being able to own their homes and being forced to rent.

At the end of the day, houses should be built for living in, not for enrichment and speculation.

There is much to be thankful for in terms of the government’s housing policy over the past several decades, but whether or not housing policy can continue to serve Singapore well is a different issue — and on this issue hinges the future of social mobility and prosperity for all.

The sentiment that “if you were born poor, it’s not your fault; but if you die poor, it is” has become a popular saying in the modern day. While there is certainly some truth to this, there are also many hidden assumptions that cannot be taken for granted, and having an even playing field is one of them.

Featured Image Credit: Reuters